This post is an excerpt from our 2023 Geography of Cryptocurrency Report, coming in October. Reserve your copy now!

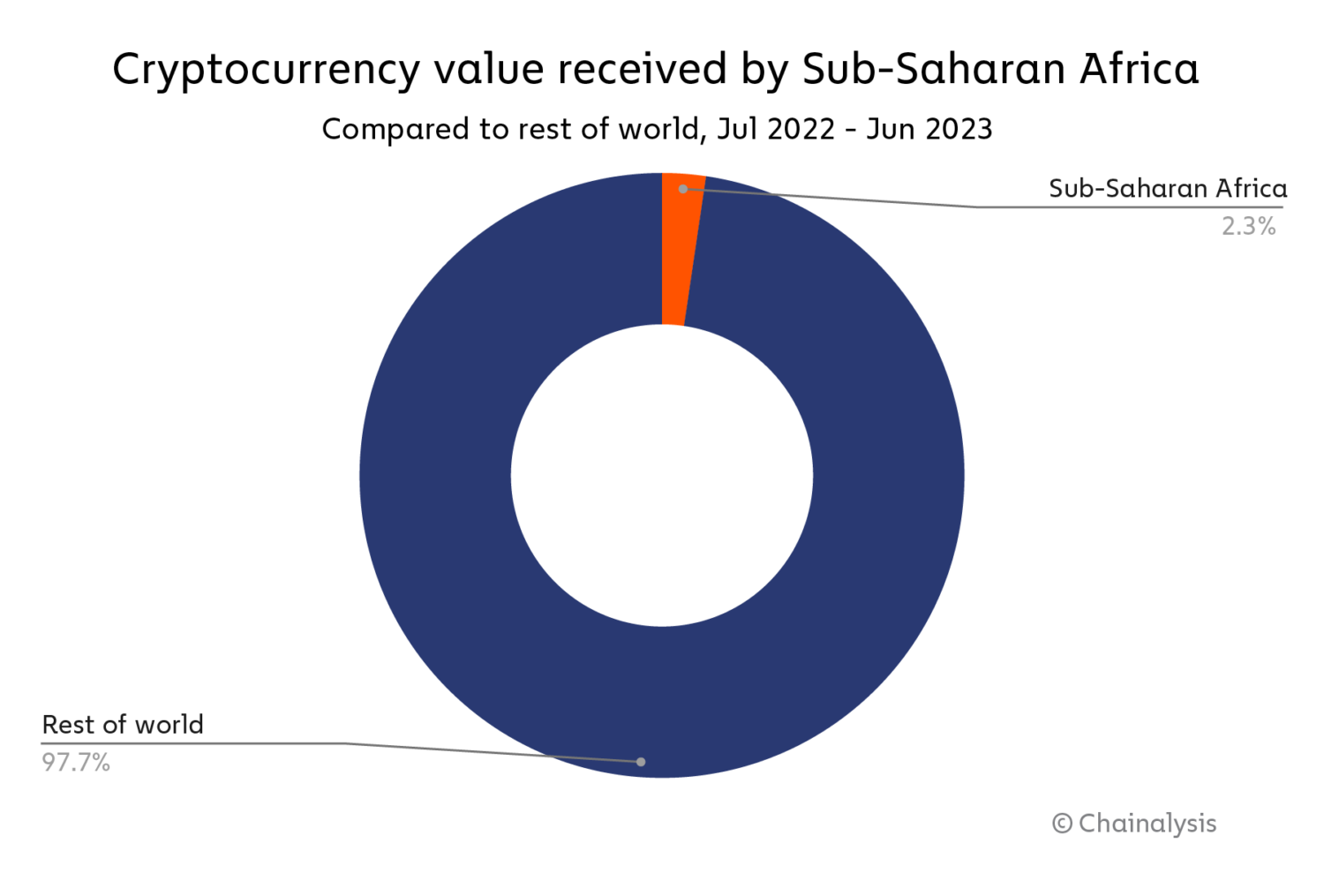

Similar to previous years, Sub-Saharan Africa has the smallest crypto economy of all regions, accounting for 2.3% of global transaction volume between July 2022 and June 2023. During that time period, the region received an estimated $117.1 billion in on-chain value.

Across the entire region during the time period studied, centralized exchanges are the most-used platform type, facilitating over half of all transaction volume. Sub-Saharan’s cryptocurrency market also appears more retail-driven than most, with a larger share of transaction volume coming in transactions under $1 million in value compared to most other regions.

Although Sub-Saharan Africa has consistently been one of the smallest cryptocurrency markets, a closer analysis reveals that crypto has penetrated key markets and become an important part of many residents’ day-to-day lives. As we’ll explore in more detail later, no country exemplifies this better than Nigeria, which ranks second overall on our Global Crypto Adoption Index and also leads the region in raw transaction volume.

Other countries in the region ranking high on the index include Kenya (21), Ghana (29), and South Africa (31). Keep reading to learn what drives crypto adoption in Sub-Saharan Africa and learn how recent regulatory developments have impacted local markets.

Citizens flock to Bitcoin and stablecoins to protect against inflation and debt

In no region is Bitcoin more dominant than Sub-Saharan Africa, as the world’s first cryptocurrency makes up a bigger share of transaction volume there than in any other region.

Why the disproportionate uptake of Bitcoin? It may be that Sub-Saharan Africa residents are turning to so-called digital gold for an alternative store of value. Many countries in the region have struggled with rising inflation and debt, making cryptocurrency an attractive means of storing value, preserving savings, and attaining greater financial freedom. In Ghana, for instance, inflation reached 29.8% in June 2022 after 13 consecutive months of increases — that marks its highest level in two decades. With relatively few financial opportunities, many Ghanians have turned to Bitcoin. Nigeria, Kenya, and South Africa have all faced similar problems in recent years, and all show a great deal of grassroots cryptocurrency adoption — that’s probably no coincidence.

However, experts on the ground tell us that some market participants have turned away from Bitcoin and towards stablecoins of late, as these generally see less price volatility than Bitcoin, whose price is well off all-time highs. Moyo Sodipo, Co-Founder and CPO of Nigeria-based cryptocurrency exchange Busha, provided some insight into this activity, stating, “When Busha gained popularity around 2019 and 2020, there was a big frenzy for Bitcoin. A lot of people were not initially keen on stablecoins. Now that Bitcoin has lost a lot of its value, there is a desire for diversification between Bitcoin and stablecoins. However, market shifts aren’t dampening activity. People are constantly looking for opportunities to hedge against the devaluation of the Naira and the persistent economic decline since COVID.”

Spotlight: Nigeria is Africa’s top crypto economy

Nigeria boasts the largest population and economy in Sub-Saharan Africa, and as discussed above, the largest cryptocurrency economy as well. Perhaps even more notable is that Nigeria’s crypto economy continues to grow despite market turmoil. In fact, Nigeria is one of only six countries in the top 50 by size globally whose crypto transaction volume grew year-over-year in the time period we studied. Its growth rate of 9.0% places it third among those six.

The evidence suggests crypto is one solution to Nigeria’s economic challenges. Since 2016, Nigeria has suffered from two major recessions, fueled by an unstable political situation, the COVID-19 pandemic, and the collapse of oil prices. Consequently, Nigerians of all ages are facing high unemployment — more than 20 million people were looking for jobs in 2021 — and many are up and moving to other countries.

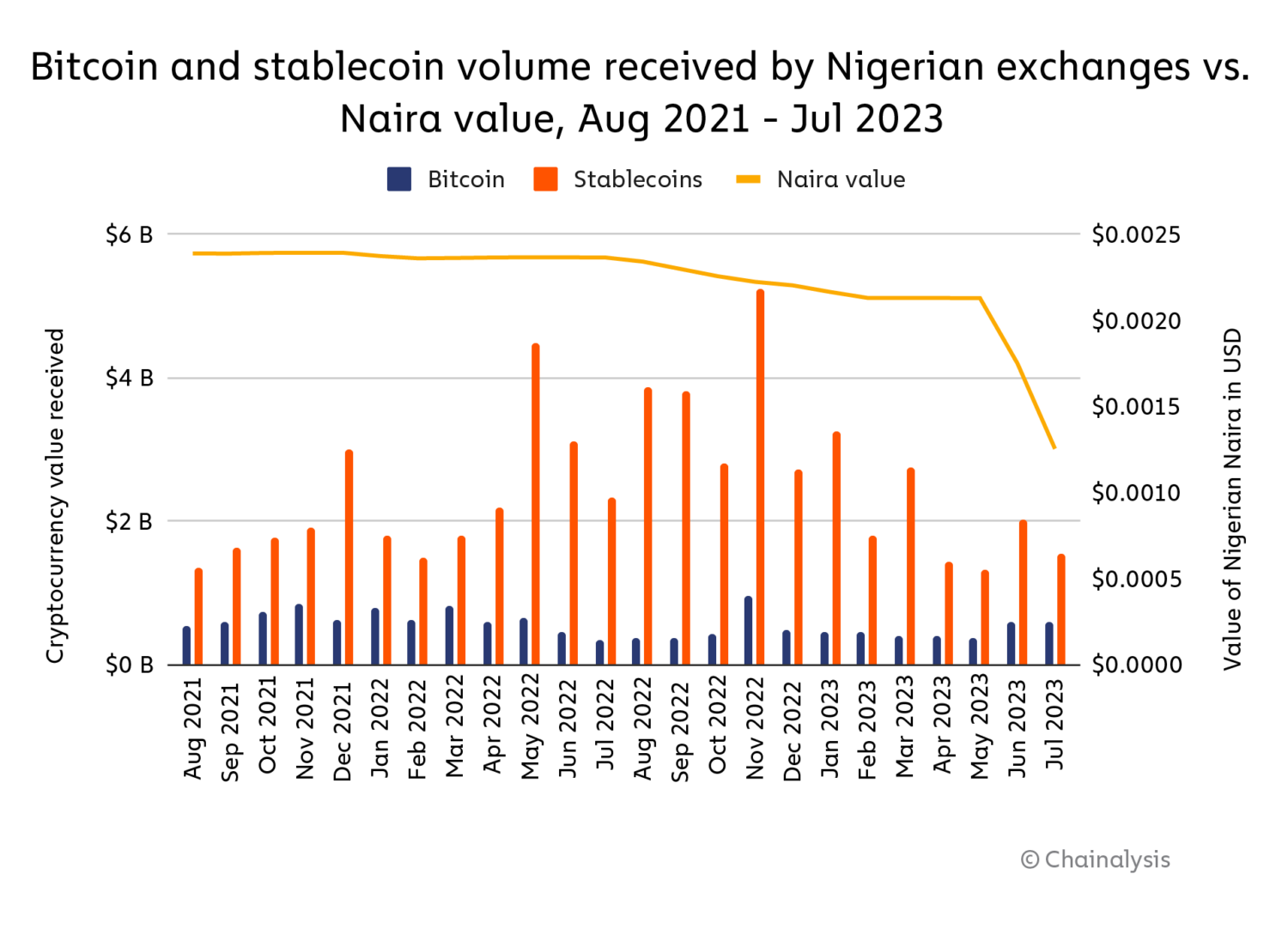

The recent Naira crisis has exacerbated these issues. In 2022, the Central Bank of Nigeria announced its intentions to redesign the Naira and issue new notes in order to combat inflation and counterfeiting, as well as take more control over how much currency is circulating.

Unfortunately, the resulting cash shortage placed enormous pressure on the country’s unbanked population and triggered uncertainty regarding the use of old notes — all during an election period and a record high inflation rate of more than 20% at the beginning of 2023. Nigeria’s uncertain economic climate has encouraged many citizens to seek financial alternatives, increasing the value proposition of cryptocurrency.

These dynamics are reflected in the data. On the chart below, we can see that interest in Bitcoin and stablecoins has generally risen as the Naira’s value has decreased, particularly during the most recent extremely steep drops in June and July of 2023. The higher spikes around May and November of 2022, however, were likely driven more by users seeking to trade on the volatility spurred by TerraLuna and FTX’s collapses respectively, as opposed to the local economic situation.

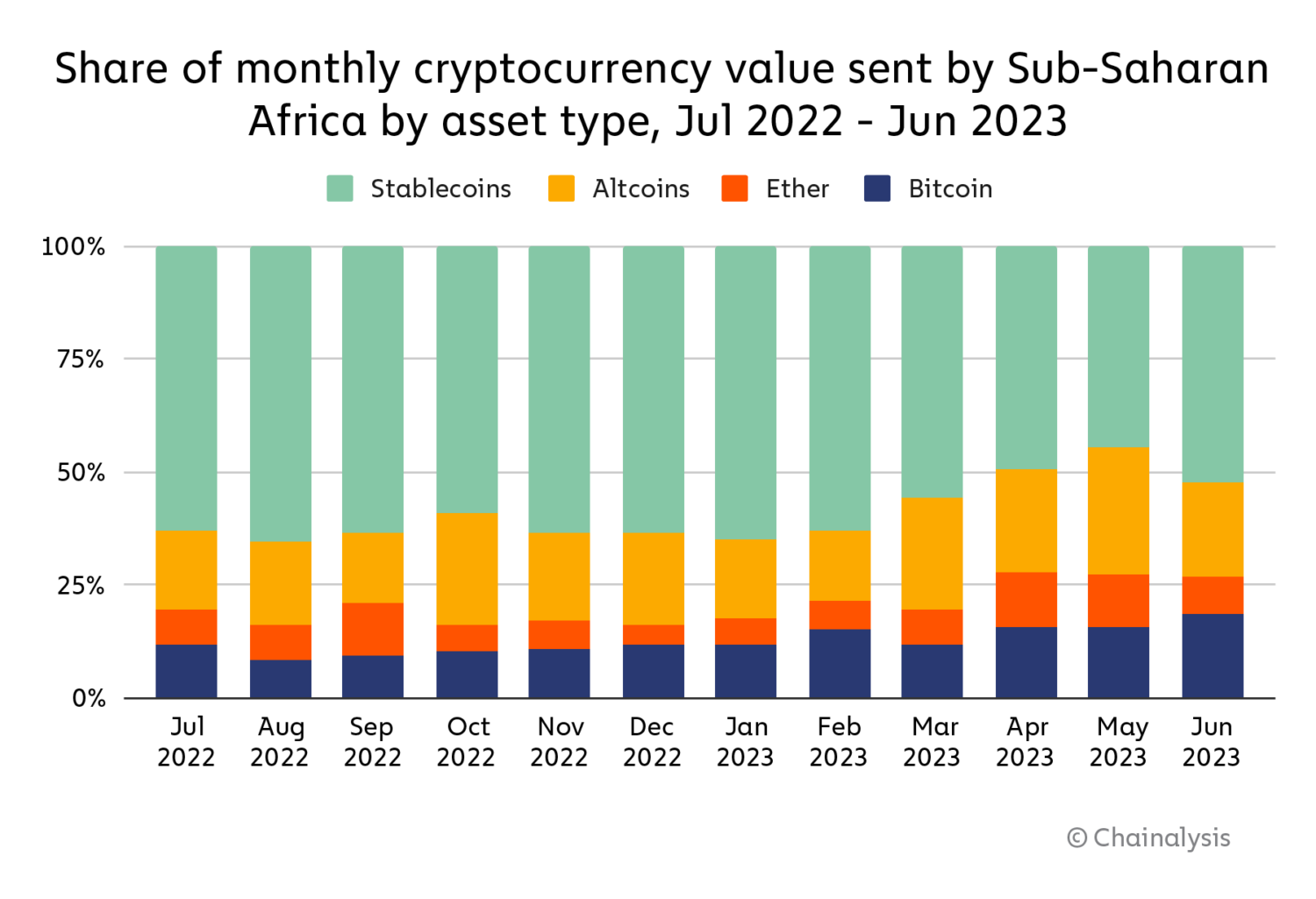

At the same time, interest in altcoins has been growing across the region lately. Moyo Sodipo explained, “On days when the market tanks, we’ve also seen a buying frenzy. It depends on the dynamics of the market at that point in time. When there is a new memecoin, like Dogecoin or Shiba, there has also been a buying frenzy. Someone is always going to be interested in a token that seems like it could make you the next couple thousand dollars.” The below chart illustrates this increase in altcoin activity, as well as the proportionally large percentage of monthly stablecoin value.

Regulatory developments throughout Sub-Saharan Africa open the door to more crypto growth

Regulation has also brought activity to exchanges in Sub-Saharan Africa. South Africa in particular has been one of the region’s leaders in terms of crypto regulation and the development of supportive trading frameworks. At the end of 2022, the Financial Sector Conduct Authority (FSCA) announced a licensing regime for cryptocurrency businesses and declared that crypto assets are financial products, lending them greater legal clarity, and also empowering financial investigators to better fight illicit activity in the space.

The country’s proactive approach to regulation has removed a lot of regulatory uncertainty and thus encouraged trading of both established and emerging digital tokens. In fact, citizens of the country have traded billions of dollars worth of digital currency in recent years. According to Marius Reitz, General Manager Africa at South Africa-based exchange Luno, “Presently, the predominant use case for crypto in South Africa revolves around investment. Over the last 3 years, the number of customers holding a meaningful crypto balance on Luno has increased by almost 50%.” He added, “In markets with no regulatory bans, we tend to see the industry develop more responsibly as the market operates above the ground, with more productive interaction between regulators and exchanges. But bans aren’t stopping people from wanting crypto. The crypto industry will continue to grow with or without regulation. It is just in everyone’s interest that there is some pragmatic regulation in place that protects consumers and creates a safer operating environment for all.”

The Central Bank of Kenya (CBK) has also been navigating the crypto landscape, issuing statements on potential volatility risks at the same time as leaders consider the implementation of a CBDC. At the beginning of 2023, the government proposed a bill advocating for a consistent securities definition of digital currencies and diligent recordkeeping by licensed crypto traders. Around the same time, the Nigerian government approved a national blockchain policy, highlighting ways blockchain adoption can benefit the country and paving the way for future legal framework.

In Mauritius, which is slightly behind Kenya in terms of raw cryptocurrency transaction volume, the Virtual Assets and Initial Token Offering Services Act of 2021 has provided comprehensive legislation for new token issuance. The country’s sustained dedication toward protecting consumers has helped promote crypto adoption and attracted traders while other countries in the region have issued explicit or implicit bans on certain crypto-related activities.

The increased regulatory clarity provided by the flurry of recent legislation may be helping Africa’s local cryptocurrency industry. As discussed above, many of the most important crypto regulations enacted by Africa’s biggest countries came around early 2023. Check out the chart below, which compares relative growth in Sub-Saharan usage of local, homegrown crypto exchanges vs. international exchanges.

The consumer safety afforded by better regulations, the confidence those regulations give consumers, and local crypto businesses’ ability to comply with those regulations may be part of why local African exchanges have been outpacing international competitors on growth within the region since early 2023.

What’s next for Sub-Saharan Africa’s crypto economy?

The future of cryptocurrency in Sub-Saharan Africa looks bright, with large countries like Nigeria already taking their place as global leaders in crypto adoption. Increasing regulatory clarity throughout the region also appears to be bolstering growth, which local crypto operators appear primed to take advantage of. The key lesson though is the same we’ve gotten from studying emerging markets over the years: While residents of wealthier nations may have buy and sell more cryptocurrency than those of emerging markets, the latter has a greater day-to-day need for cryptocurrency, very much in line with the original vision for Bitcoin and the sector at large.

This material is for informational purposes only, and is not intended to provide legal, tax, financial, or investment advice. Recipients should consult their own advisors before making these types of decisions. Chainalysis does not guarantee or warrant the accuracy, completeness, timeliness, suitability or validity of the information in this report and will not be responsible for any claim attributable to errors, omissions, or other inaccuracies of any part of such material.